Affordable house pricing has been an issue for as long as most of us can remember. Our grandparents bought their first homes when their annual salaries were just a shade less than the purchase price. By the time the 80s rolled around, the difference was much more stark, it was likely a home could be twice the annual salary but when the 90s hit and interest rates, already at record levels of 12% surged forward to 17.5% it looked like nothing could ever be worse.

But worse it is, interest rates eased back but the prices of homes did not. People might argue that the current interest rates are nowhere near the levels encountered in the 90s and that’s true but we’ve seen one increase after another, 8 in 12 months, by USA’s Fed and 11 in a row by the Reserve Bank in Australia. Rates are now at a 16 year high in both countries and, despite being a lot lower than the 90s, other conditions make it a much worse for homeowners than it was 30 years ago.

What’s changed for the buyer are two things: one is the cost of houses; the other is average incomes didn’t keep pace with inflation. Even though interest rate levels are only about a third of those of the 1990s, the price of a home has risen from 2.5 times the average annual income at that time to 5.3 times the average income. In other words, those houses and apartments in 1990 were, even with rising 12% interest rates, still affordable to the average buyer, now they are not.

But there’s more, relaxed banking laws have allowed more people to borrow more money than they could 40 years ago and, according to some sources, more than 25% of all current loans are risky loans. Meaning investing in banks could be a risky business (particularly, as we’ve seen, in the USA).

Australia’s Parliament House Library tells us that “housing stress” kicks in when we’re paying 30% or more of our income to cover our accommodation. While there appears to be some light at the end of the tunnel in the USA, the opposite is true for Australia, according to SGS Economics, there are currently 640,000 low-income Australian families experiencing housing stress and this is scheduled to increase to at least a million homes.

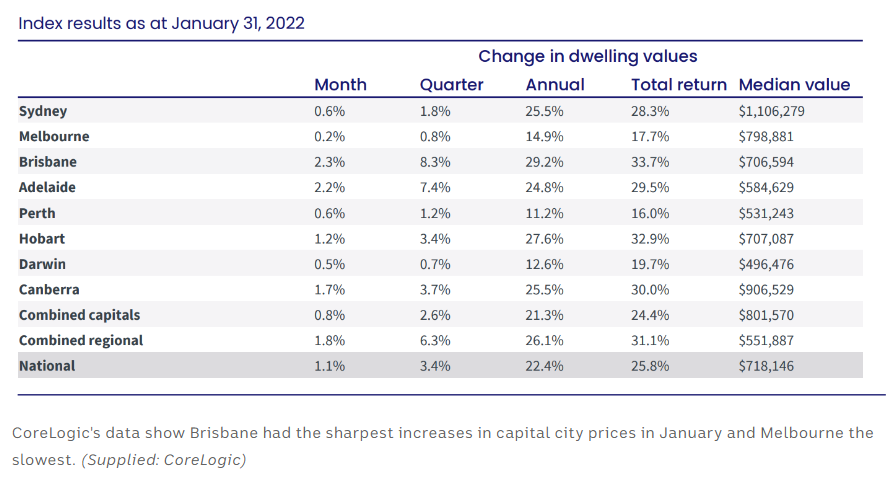

In Australia, wages increased 3.8% during 2022 while inflation (CPI) rose through 2022 to a high of 9% but home prices in some cities for the same period increased by as much as 29% but with a national average of 22% growth during the same period.

This combination of declining real-level incomes, higher loan amounts as well as the now increasing costs to service those loans impact not just on the individual home buyer, but on the health of the economy.

Australia’s most popular retailer is the hardware store Bunnings, it reported record revenue and earnings in 2022 as people, confined to homes, completed those long awaited DIY projects. But Woolworth’s the number one performing supermarket chain recorded “below aspirations” slower growth, managing to post $1.5 billion dollars in profit despite Covid issues and product shortages due to floods in two states while, at the same time, pointing to a reduction in sales of beef and fresh vegetables due to customers buying less of these as prices increased and cash-strapped consumers switched to cheaper, tinned and frozen, foods.

While it’s clear there is justifiable concern for home owners, the Aussie battler, as media likes to call them, there is an even great concern for the global economy overall as a variety of factors impact. The US Fed has indicated it isn’t over yet but is likely to ease off interest rate increases with a pause in June, it’s likely Australia will follow suit but signs are ominous: Bitcoin is down for the first time in two months, Wall Street, London’s Stock Exchange and Australia’s Stock Exchange are all also down.

The US Fed targets getting inflation back to 2% but it currently, and stubbornly, remains higher at 4.9%. This means there could well be more rate increases, as Jerome Powell indicated during a recent Senate hearing.

Increasing interest rates should cool spending; cooling spending should decrease inflation but decreased spending also leads to less demand, which turns into higher unemployment. All of this bodes poorly for new and prospective homeowners.

The economic environment globally, is further complicated by recent US bank collapses, which some pundits predict will continue, and the possibility of a US debt default, which the world expects will be averted, either by a political compromise or by invoking the 14th amendment. Either way, both of these options increase the likelihood that interest rates will rise further.

{kind=link}